In this article, we will be looking at debt sculpting in project finance modeling.

The concept of “Debt Sculpting” is extensively used in project finance transactions and financial modes for project finance transaction evaluation.

Debt sculpting is essentially a calculation of debt repayment schedule in such a way, that debt service is tailored to the strength and pattern of the cash flow that the project generates.

One of the key ratios that lenders use to analyze the project’s ability to repay the debt is the debt service coverage ratio, or, DSCR.

DCSR is a ratio generated by the project, and then, the project’s DSCR is compared to the DSCR required by the lenders.

Often, you may encounter a situation in project finance, with level or annuity debt repayment profile, when the weighted average DSCR generated by the project is larger than the minimum required DSCR, however, periodic DSCR in some periods may be lower than the minimum required DSCR.

In other words, the total project’s cash flow may be more than enough to repay the debt, however, due to unusual, one-off payments such as the major overhaul of the project in some periods, the periodic DSCR may be lower than the minimum required DSCR in those periods.

Debt sculpting is generally applied when a project has irregular, but well-understood cash flows, for example:

- inoil&gasprojects,

- or because of the seasonal demand factors, which is common in the power industry,

- or because of an unusual but expected payment, such as a major overhaul of an asset.

So how do we do the debt sculpting in financial modeling for project finance transactions?

Let’s start with DCSR definition, which is a ratio of CFADS to debt service. What we want to do when we are tailoring debt service to CFADS, is to maintain the same DSCR in all periods when we have to pay debt principal and interest.

We achieve this by rearranging this DSCR formula – divide CFADS by the DSCR to get the debt service, which is the sum of debt principal and interest payments.

We can further rearrange this formula to get to the debt principal repayments – which is CFADS divided by the DSCR and then, we have to subtract the interest expense.

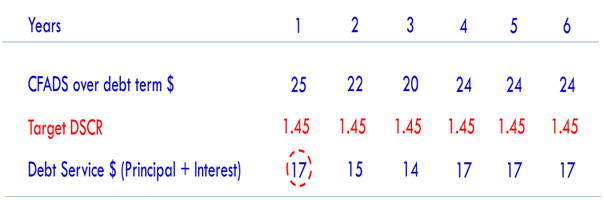

So, let’s work through an example of debt sculpting. First, let’s assume that we have 6 years. We have our CFADS over debt term, and, our target DSCR is 1.45. Target DSCR is the same as the required DSCR by the lenders. Check out other articles by FMO – Financial Model Online on debt service reserve account https://www.financialmodelonline.com/blog/220314/dsra

So, let’s work through an example of debt sculpting. First, let’s assume that we have 6 years. We have our CFADS over debt term, and, our target DSCR is 1.45. Target DSCR is the same as the required DSCR by the lenders. Check out other articles by FMO – Financial Model Online on debt service reserve account https://www.financialmodelonline.com/blog/220314/dsra

Next, to get the debt service in Year 1, we have to divide the CFADS by the target DSCR. So we have our debt service.  Assume, that our initial debt balance is 75 which carries an interest rate of 7.5%. So, the next step is to calculate the interest expense, which is the debt opening balance multiplied by the interest rate of 7.5%.

Assume, that our initial debt balance is 75 which carries an interest rate of 7.5%. So, the next step is to calculate the interest expense, which is the debt opening balance multiplied by the interest rate of 7.5%.  Now, we can subtract from the debt service the interest expense to get to the debt principal repayment. And, based on the debt opening balance and principal repayment, we get to the debt closing balance in Year 1, which is the debt opening balance in year 2. Please note that the numbers do not add up due to rounding. So we repeat this exercise until we fully repay the debt and our debt closing balance is equal to zero.

Now, we can subtract from the debt service the interest expense to get to the debt principal repayment. And, based on the debt opening balance and principal repayment, we get to the debt closing balance in Year 1, which is the debt opening balance in year 2. Please note that the numbers do not add up due to rounding. So we repeat this exercise until we fully repay the debt and our debt closing balance is equal to zero.  Now you can see that variation in our debt principal repayment, and debt service, follow the variations in our cash flows available for debt service. When our cash flow is high, our debt service is high, and when our cash flow is low, our debt service is low. In this article, we learnt about the debt sculpting in project finance transactions. To learn about financial modelling for project finance please enroll in our courses:

Now you can see that variation in our debt principal repayment, and debt service, follow the variations in our cash flows available for debt service. When our cash flow is high, our debt service is high, and when our cash flow is low, our debt service is low. In this article, we learnt about the debt sculpting in project finance transactions. To learn about financial modelling for project finance please enroll in our courses:

Project Finance Modeling for Infrastructure Assets – https://www.financialmodelonline.com/p/project-finance-modeling-course Project Finance Modeling for Renewable Energy – https://www.financialmodelonline.com/p/project-finance-modeling-for-renewable-energy